[Introduction] In the traditional peak demand season of “Golden Nine and Silver Ten”, the start-up of polyester filament and terminal textile industries has passively declined. On the one hand, the global epidemic has not yet been fully controlled. Although it is the peak season, overseas orders have not shown a growth trend. On the contrary, some weaving companies have reduced orders. External demand is sluggish, while domestic companies have high inventory of finished products and low production enthusiasm. On the other hand, under the influence of dual control, The operating load of the texturing, weaving, printing and dyeing industries in Changxing, Jiaxing, Shaoxing and other places has dropped. Domestic demand is insufficient, and the supply pressure of the polyester filament industry has become prominent. A mode of load reduction and risk aversion has also been launched recently.

Figure 1 Comparison of production starts in polyester filament and downstream fields in 2021

Source: Longzhong Information

As shown in the figure above, the start of polyester filament production in the first half of the year was much higher than the same period last year, but compared with 2019, currently The operating rates are all at a low level, and since August, corporate inventory pressure has continued to grow. Leading companies have taken the lead in reducing burdens and avoiding risks, and the operating rate has dropped sharply since the middle of the year. Since September, due to the influence of the national dual-control policy, high-energy-consuming enterprises such as printing and dyeing, weaving, texturing, and polyester have gradually reduced their production volume in accordance with relevant local policy requirements. In mid-September, polyester filament yarn began the second round of negative pressure reduction, and many Sets of equipment have been shut down one after another, and the industry’s start-up has dropped to around 80%, which is far lower than the level of the same period last year.

The current factors affecting the start-up of the polyester filament and terminal weaving industries are mainly divided into two aspects: First, the decline in demand has led to increased inventory pressure on enterprises, and enterprises have reduced their burdens to Alleviating inventory pressure, however, the reduction in supply is not as strong as the contraction in demand, and excess supply has forced the industry to start a decline. Specifically, under the influence of the epidemic, polyester filament exports have continued to decline since April. Affected by negative factors such as skyrocketing sea freight and container shortages, the resistance to textile and clothing exports has also gradually increased. According to customs data, in January 2021 -In August, textile exports totaled US$92.8232 billion, -11.44% compared with the same period last year. Since the second quarter, after the delivery of early orders, new orders for polyester filament and terminal textiles and apparel have been slow to be placed. Some manufacturers have reported that there have been few orders from Europe and the United States since April. External demand is sluggish, domestic demand is insufficient, and demand has dropped significantly. The current epidemic situation at home and abroad is still severe. According to official data from the World Health Organization, as of September 21, 2021, about 43.7% of the global population has received at least one dose of vaccine. In low-income countries and regions, only 2% Have had at least one dose of vaccine. Even in China, when the overall epidemic situation is under good control, new cases are still emerging in many places, which has affected logistics, transportation, production and sales to a certain extent. Coupled with the current sluggish demand, the inventory pressure of polyester filament and terminal textile and clothing companies is gradually increasing. The supply contradiction has intensified, forcing the industry to start a decline.

Figure 2 Overall inventory comparison of the polyester filament industry from 2019 to 2021

Source:LongzhongInformation

Duetothegreaterimpactoftheepidemicin2020,itisnotusedasreferencedata,asshowninthefigureAsshownin2,polyesterfilamentyarnsshowedadestockingtrendfromAugusttoSeptember2019.Throughouttheyear,theoverallinventoryoftheindustrywasmostlycontrolledwithinhalfamonth,whichisanormallevel.In2020,ontheonehand,duetotheimpactoftheepidemic,enterpriseshaveaccumulatedinventory,ontheotherhand,newproductioncapacityhasbeenputonthemarket,increasingsupplypressure.Since2020,polyesterfilamentinventoryhasremainedhigh.Drivenbythecostsidefromtheendoflastyeartothebeginningofthisyear,thepriceofpolyesterfilamentcontinuedtorise.Undertheguidanceoftherisingbuyingatmosphere,endusersconcentratedonstockingup.Theinventoryofpolyesterfilamentfelltoalowlevelatthebeginningoftheyear.However,asdemandcontinuedtodecline,inthefirsthalfoftheyearThenewlyaddedproductioncapacityofnearly2milliontonsperyearhasfurtherintensifiedthesupplypressureoftheindustry.Sincethethirdquarter,theinventorypressureofpolyesterfilamenthascontinuedtoincrease.AsshowninFigure3,theinventoryofrawmaterialsandfinishedproductsintheweavingindustryhasalsoshownavolatileupwardtrend,especiallysinceJuly.Theinventoryofwovenproductshasincreasedsharply,andsomesmall-scaleenterpriseshavesuccessivelyreducedandstoppedequipmenttorelieveinventorypressure.

Figure3Polyesterfilamentandterminalweavinginventorycomparisonin2021

Source: Longzhong Information

Before the dual control, supply pressure caused the polyester filament and terminal fields to start production reduction mode. Since September, the dual control policy has had a greater impact on many places in Jiangsu and Zhejiang. The operating loads of polyester filament, texturing, weaving, and printing and dyeing have all declined to varying degrees, which is the second factor affecting the start-up of the industry.

In mid-August, the “Barometer of Completion of Dual Energy Consumption Targets in Various Regions” released by the National Development and Reform Commission in mid-August showed that in terms of energy consumption intensity reduction, including Jiangsu The energy consumption intensity of nine provinces (autonomous regions) including China rose instead of falling in the first half of the year, which is a first-level warning. In terms of total energy consumption control, eight provinces (autonomous regions) including Jiangsu, Fujian, and Guangdong are in first-level early warning, and Zhejiang, Anhui and other provinces (autonomous regions) are in second-level early warning. The main textile production areas are mainly concentrated in Jiangsu, Zhejiang, Fujian, Guangdong, Anhui and other places, so the impact of dual control will have a greater impact on the textile and clothing industry.

It is true that at the end of 2020, epidemics also occurred in many places in Zhejiang.� News on energy conservation, emission reduction, and power rationing policies, such as “Tongxiang launches city-wide dual energy control and coal consumption reduction A-level emergency response”, “Hangzhou promotes energy conservation”, “Power outages in factories in counties and cities in Jinhua, Zhejiang Province” Energy conservation and emission reduction have begun”, “Zhejiang Cixi chemical fiber enterprises will limit power supply for 2 days before the end of this month”…According to verification, for the polyester industry, texturing enterprises have a greater impact, because texturing machines consume large amounts of electricity. , therefore affected by the policy, many texturing companies in the region have appropriately shut down some texturing machines. Recently, due to the high profit level of texturing, the operating load of the texturing machines is mostly above 95%. Affected by this policy, it is expected that The startup load of the local texturing machine has dropped to around 80%. The power limit period of this policy is from mid-December to the end of the month, so it has limited impact on the polyester filament and terminal textile industries. From the end of December to mid-January of the following year, many companies in the Xiaoshao area planned to shut down due to boiler renovations, and the supply of polyester was reduced. Most polyester factories said that texturing machines maintained normal operation, and terminal demand declined at the end of the year, so the overall The supply and demand pattern has not changed significantly yet, mainly affecting the supply of POY and FDY. However, boosted by this news, the overall supply of polyester has shrunk, giving certain support to market prices. This year, dual-control management in many places in Jiangsu, Zhejiang, Anhui, and Guangdong has been relatively strict. Some local high-energy-consuming devices have been gradually reduced and shut down, and the start-up of polyester filament and terminal fields has dropped significantly.

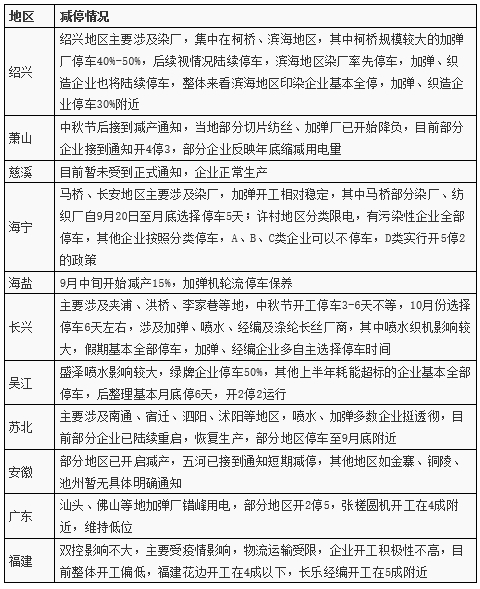

Table 1 Summary of device reduction and suspension in major regions

Note: The above content is a summary of industry research and is for reference only

Recently, under the power consumption control of high-energy-consuming enterprises, most enterprises during the Mid-Autumn Festival plan their parking accordingly. . Among them, texturing, weaving, and downstream dyeing plants are mainly involved, and the shutdown rate of weaving companies and dyeing plants is higher than that of texturing companies. Currently, the parking time of most downstream weaving enterprises is 3-6 days, and the parking time of the higher ones is until the end of the month. The second phase of parking arrangements may be implemented in October. Specific to each loom type, the current operating rate of water-jet loom companies in Shengze, Changxing and Siyang has dropped significantly. Among them, the Changxing water-jet loom has dropped to around 10%, and the water-jet loom companies in Siyang and Shengze have both declined. fell by 8-12 percentage points. The startup rate of Xiaoshan Shaoxing circular knitting machine and Foshan Zhangcha circular knitting machine itself is relatively low, with partial power cuts or a two-day shutdown. The impact is smaller than that of other production bases, and the startup rate has not changed much compared with last week. Although the warp knitting industries in Changshu, Haining and Changle have a partial holiday of 1-2 days during the Mid-Autumn Festival, they have now restarted, and the operating rate has only dropped slightly, remaining at around 70-80%. Xiamen and Putian in Fujian are affected by the epidemic, and logistics Restricted, shipments are blocked.

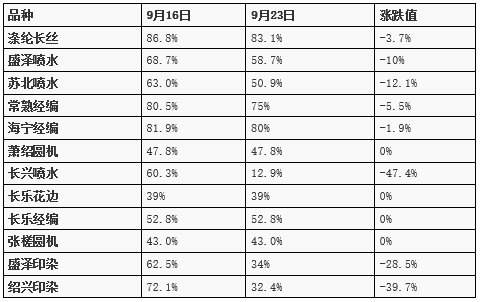

Table 2 Comparison of loom and printing and dyeing operations of polyester filament and major downstream regions

Source: Longzhong Information

As shown in the table above, this round of power cuts has a greater impact on the downstream weaving, printing and dyeing industries. The weaving industry mainly involves water-jet looms. The overall impact of warp knitting and circular knitting machines is currently relatively small. The demand side has shrunk sharply, which has highlighted the supply contradiction of polyester filament. In the short term, there are still expectations for promotion of polyester filament on the eve of the National Day holiday. In the medium and long term, the polyester filament industry will also face further production cuts.

</p